The Life-Changing DeFi Tool Everyone Should Be Using

The Life-Changing DeFi Tool Everyone Should Be Using

First off, thank you for reading and as always, nothing you read or hear of my content is ever financial advice. It is simply content to help you think more about the ever changing landscape of finance/technology and where I believe we are headed in the future.

My goal in creating this Substack/Twitter (follow me @CryptoOnramp) is to onramp 100+ people into crypto through easy to understand descriptions of the various new technological concepts, so I would appreciate it if you could please subscribe and share if this article hits the spot!

This content is intended to provide a high level overview of concepts for beginnings looking to enter the space. If you are looking for more in-depth analysis regarding anything written below, I would strongly suggest creating a Twitter account and joining the Crypto Twitter space. Start by following a few of the same people that I do on @CryptoOnramp, or reach out to me via DM and I can suggest a few educational resources to dive deeper into the wide world of Web 3, crypto, and blockchains!

You have probably heard of the term decentralized finance, or “DeFi” for short, but what does it actually mean, and why are some people predicting that the technology will change finance forever?

In this article, instead of tackling the whole space at once and overwhelming someone who may have 0 background knowledge, I will provide 1 simple example of DeFi to show it’s limitless potential in taking power (and profits) away from large financial institutions (such as JP Morgan, Bank of America, etc) and giving it back to you!

You’ll also start to realize why these same financial institutions feel threatened by its potential, and continue to say negative things about DeFi. After all, if you knew something was inevitably going to eat your lunch, you would do everything you could to stop it from happening as well!

The 1 simple example relates to trustless and permissionless lending.

But what exactly does that mean?

Currently, if I would like to borrow money for any reason (buy a home, car, start a business, invest), the most likely path that I would take is to approach my bank. This is the path where the majority of lending happens in the form of mortgages, lines of credit, etc.

But how does the bank have enough capital to lend to me?

To simplify this process in layman’s terms, the bank takes all of the total deposits from everyone who is a customer at the bank, and is only required by law to hold a certain percentage as cash at all times. This can range anywhere from 3% to 25% depending on where you live.

This means for every $100 deposited into a bank in an individual’s chequing or savings account, the bank only has $3-25 worth in cash available for you to withdraw.

What do they do with the other $75-97? They lend it out to people as loans and collect interest on it, which becomes a revenue stream for the bank!

Now a quick comparison will show how unfair this system actually is, yet we are confined to it because there are (were) not realistic alternatives.

You deposit $100 into your savings account at your local bank. The bank pays you an interest rate of 0.01% (screenshot taken as at Dec 7 from TD Canada’s website)

TD then turns around and loans out the 75-97% of that $100 they are not required by law to hold in cash to someone who is looking for a loan.

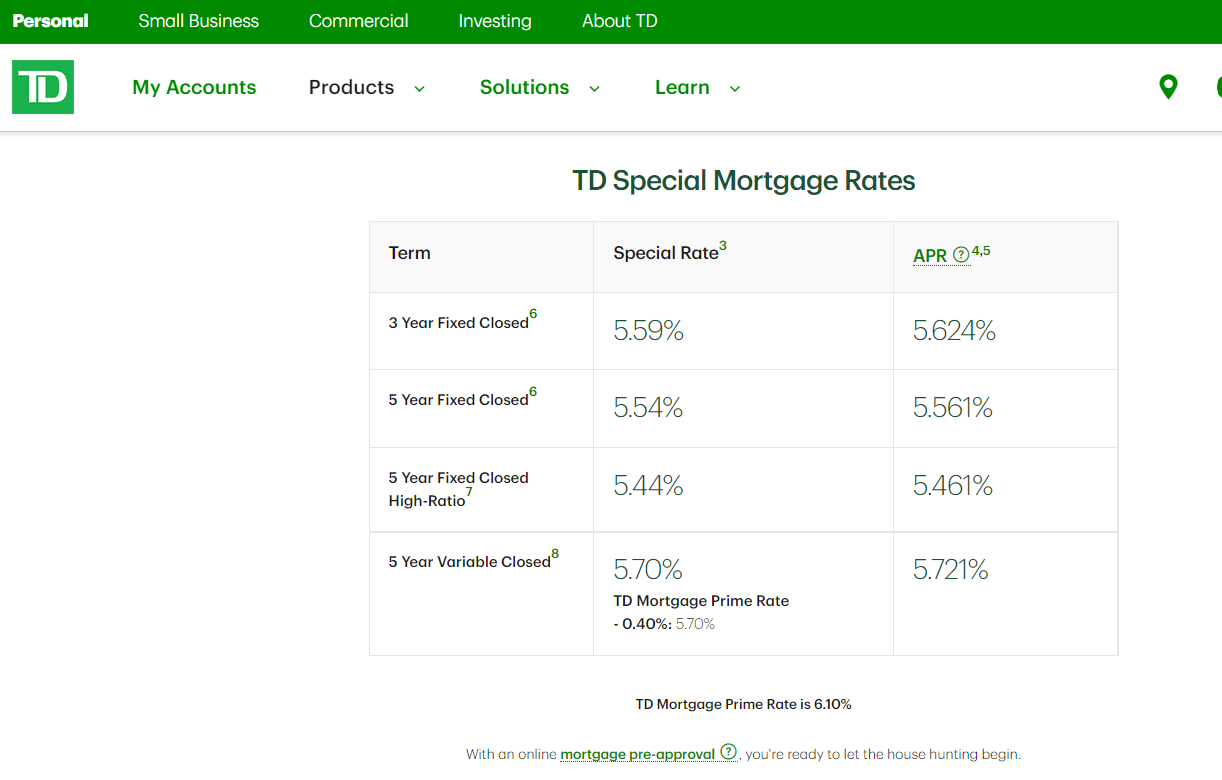

Let’s say your friend is looking for a mortgage from TD to purchase a new home. They would then apply for a mortgage with the below interest rates (screenshot taken as at Dec 7 from TD Canada’s website):

Even picking the lowest mortgage interest rate, it is easy to see that TD makes a pretty decent amount off of your $100 deposit, 5.43% to be exact (5.44% less 0.01% they need to pay you).

Using this basic example, it’s pretty easy to see how TD amassed a net profit in fiscal 2022 of $15.5 billion dollars!

Of course, there are several things that a bank provides to an individual which would incentivize deposits, including safely storing funds, access to widely accepted payment methods, etc.

However, it quickly becomes evident that another company uses your funds to generate profit, without you seeing any part of that.

Wouldn’t it be nice if your friend who was looking to borrow money to buy a home at 5.44% could approach you currently earning 0.01% and split the difference, with both parties benefiting, and the 3rd party (TD in this case) not being able to profit off of the both of you?

To date, there has not been any way for the individual to take advantage of a better system, as a centralized banking institution provide a trusted source regulated by the government for individuals to safely borrow and invest funds.

With the creation of blockchain and smart contracts, we now have access to additional methods, including direct lending and borrowing.

For simplicity’s sake, I will use the largest lending/borrowing protocol in existence (AAVE) as an example.

How AAVE works:

AAVE is a trustless and permissionless peer-to-peer (or peer-to-pool) lending and borrowing platform in which users can deposit cryptocurrency assets to be borrowed against in exchange for a share of the borrowing costs.

Simply put, I can deposit $100 worth of Bitcoin, Ethereum, USD stablecoin or a variety of other tokens, and collect interest off the platform. Users also can borrow from AAVE in exchange for paying an interest rate.

As AAVE is a trustless and permissionless protocol, all loans are fully collateralized, and an individual can only borrow up to a certain percentage of their deposits. This percentage usually ranges around 75%, as in depositing $100 will allow you to borrow up to $75. No repayments are necessary as long as you can maintain a borrowing ratio of less than 75%, unlike banks that usually require monthly repayments.

Since crypto prices are extremely volatile and users can deposit tokens that are not stable, the AAVE smart contract automatically liquidates any positions that exceed this 75% ratio, by selling enough of the assets deposited in order to pay back the loan borrowed.

Therefore, it isn’t recommended or smart to actually borrow 75% of your assets.

As this process is governed by a smart contract and is not done by an individual, it is important to note that AAVE and other smart contract DeFi lending protocols functioned exactly as intended during the VC liquidations of the 2022 crypto crash, and did not lose a penny of money for anyone else.

It was impossible for a VC firm to borrow money from AAVE without providing the asset collateral up front. However, VCs were also able to borrow money from other companies based on their reputation without having to fork over any collateral, which inevitably meant millions in losses when they were unable to pay back the loans.

With AAVE, as $BTC and $ETH price dropped, these VC firms were required to provide more collateral into the system to ensure their loan ratio was in compliance (below 75%). When they were unable to do so, the smart contracts automatically liquidated their assets in order to repay the loan.

Looking at the protocol platform, the rates can be very lucrative in comparison to a traditional bank such as TD (screenshot taken on Dec 7):

A USD pegged stablecoin such as USDC currently pays out 1.27% aPY in interest compared to TD at 0.01%. USDC can also be borrowed at a variable rate of 2.48%, which is significantly lower than any rate you can find at any bank.

Given the cryptocurrency ecosystem is currently in a bear market and rates are based on supply and demand, these supply aPY rates are some of the lowest on record since AAVE’s invention. As crypto continues to gain mainstream adoption, there will be more demand for services such as AAVE, and aPYs will increase.

Simply put, a user is willing to pay 10% to borrow if they can use it to invest in something that will pay them 25%, and if someone is willing to pay 10% to borrow, the amount paid to the lender increases.

Now that you understand the basics of a lending/borrowing protocol such as AAVE, let’s take a look at 2 of the biggest benefits of this function of DeFi versus its traditional finance (TradFi) equivalent:

Wealth-Building:

One of the simplest forms of wealth building is to abide by the following concept:

“Never sell an appreciating asset.”

However, it is very difficult for the majority of us to live by this principle. We largely trade our time to earn dollars at a 9-5 which is then used to purchase goods/services that we consume, and don’t have enough funds leftover to purchase assets such as investments, leaving us stuck in the proverbial “rat race”.

There are methods available in which an individual can follow this concept, such as owning a business or purchasing a home and taking out a home equity line of credit against it, but these methods require a significant amount of up-front capital and approval (which we will cover next).

With AAVE, an individual can take any amount of money, whether it be $10, $100, $1,000 or more, purchase an asset that will theoretically appreciate over the course of time such as Bitcoin or Ethereum, and then borrow against it.

Let me use a quick math example to demonstrate the difference in wealth building:

Sally collects $1,000 of pay from her 9-5 job, and uses $500 of that amount to purchase groceries for the week. Sally is left with $500.

Billy collects $1,000 of pay from his 9-5 job, invests the full amount into Bitcoin, deposits it onto AAVE, and borrows $500 to pay for groceries. Bitcoin subsequently goes up 25%, bringing Billy’s Bitcoin value to $1,250. Billy’s net worth in this scenario is $750.

Billy’s net worth is $250 more than Sally’s.

Of course, there are many caveats to the example demonstrated above, including interest rates and the massive volatility in Bitcoin price that may force Billy to add more collateral in order not to get liquidated, but hopefully this provides a basic scenario in which it would be beneficial to never sell an appreciating asset (but rather borrow against it) if you don’t have to.

With AAVE and cryptocurrency, the option exists for individuals at any income level to start accumulating wealth.

Reread that sentence.

Individuals at ANY income level to start accumulating wealth. Sadly, that is not a realistic reality with the current traditional financial system.

Permissionless Borrowing

Despite the many different banking institutions in which an individual can borrow money, they all require an application, and there are still several reasons why someone may be denied:

Not enough annual income

Bad credit history

Previous bankruptcies

Lack of ID/documentation

This often leads to a number of individuals being turned away despite having the ability/capacity to pay back the loan.

With AAVE, borrowing is trustless and permissionless. It does not depend on an individual at the bank to provide approval. If you have the adequate assets and want to take on the risk, you can take out the loan!

Simple as that.

There are still a number of things that need to be figured out for this technology to be mass adopted, including the ability to perform uncollateralized loans (which banks do very well, although in theory they collateralize your earning power instead), tokenization of real world assets such as land and stocks so that there are more assets to choose from other than cryptocurrency, etc.

Admittedly, we are in the 1st inning of this new innovation.

However, given the information provided above, it isn’t difficult to see why DeFi lending/borrowing is going to inevitably overtake and phase out traditional borrowing through centralized banking institutions.

It is only a matter of time.

The question is, will you be in a position to take back control of your own wealth when the time comes? Or will you continue to let traditional financial companies profit off of you?

The choice is yours.

Choose wisely. #DeFi